Please note: While we live and breathe Non-QM, we know the bigger picture matters. This update looks at the broader mortgage market because what’s happening out there impacts everyone—borrowers, brokers, and lenders alike.

Mortgage rates moved to their lowest levels since mid-May this week, giving borrowers and mortgage brokers some welcome relief.

But the bigger question is not just whether rates moved lower.

It is why rates improved — and what brokers should be watching next.

Right now, oil prices, inflation expectations, Treasury yields, and labor market data are all playing a role in where mortgage rates go from here.

Let’s break it down.

Why Lower Oil Prices Matter for Mortgage Rates

One of the biggest reasons rates improved recently is the decline in oil prices.

After earlier concerns about supply disruptions tied to tensions in the Middle East, crude oil has fallen back toward the $70 per barrel level.

That matters because oil impacts inflation.

When energy prices rise, costs tend to move through the economy in several ways:

- Transportation becomes more expensive

- Manufacturing costs increase

- Shipping costs rise

- Food and consumer goods can become more expensive

When oil falls, the opposite can happen over time.

Lower energy costs can help reduce inflation pressure, which is generally positive for bond markets and mortgage rates.

Broker takeaway:

Oil prices may seem far removed from housing, but they can have a direct impact on inflation expectations — and inflation expectations are a major driver of mortgage rates.

Diesel Prices Are Also Important

Diesel fuel is another key piece of the inflation story.

Diesel impacts nearly every part of the supply chain, including farming, trucking, manufacturing, and grocery distribution.

With diesel prices near their lowest levels since 2021, businesses may see some cost relief over time.

That is important because lower supply chain costs can help reduce inflation pressure throughout the economy.

Broker takeaway:

Lower diesel prices may not show up in mortgage rates overnight, but they can support a better inflation outlook if the trend continues.

Why This Helps the Fed

Lower oil prices also matter for Federal Reserve policy.

If energy prices continue to fall, it may reduce the risk of inflation reaccelerating.

That could make it easier for the Fed to remain patient instead of considering additional rate hikes.

For brokers, this is important because Fed policy expectations influence the bond market, and the bond market plays a major role in mortgage pricing.

Housing Supply Is Getting Attention

Congress also passed a housing package aimed at addressing affordability and inventory challenges.

While new housing legislation will not solve supply issues immediately, it is an important development because housing affordability is not only about rates.

It is also about available inventory.

More supply over time can help:

- Create more options for buyers

- Ease affordability pressure

- Support a healthier housing market

- Improve long-term purchase opportunity

Broker takeaway:

Rate movement matters, but inventory matters too. More housing supply could create more opportunities for buyers and brokers over time.

The 10-Year Treasury Trend Is Worth Watching

The 10-year Treasury briefly touched 4.69% about six weeks ago.

Since then, yields have moved lower toward the 4.40% range.

That trend has helped support mortgage rate improvement.

Historically, the 10-year Treasury has struggled to stay above 4.60% for long periods. The last time it moved above that level and stayed there for 90 days or more was back in 2008.

That does not guarantee rates will continue lower, but it does suggest that the recent peak in yields may be difficult to sustain.

Broker takeaway:

The 10-year Treasury remains one of the most important indicators brokers should watch. When Treasury yields move lower, mortgage pricing often follows.

What This Means for Your Pipeline

This kind of market creates opportunity — but only for brokers who stay proactive.

- Revisit Borrowers Who Paused

Borrowers who were waiting on the sidelines may be more open to conversations now that rates have improved.

This is a good time to reconnect with:

- Pre-approved borrowers

- Rate-sensitive buyers

- Suspended files

- Borrowers who paused due to affordability

- Educate Borrowers on Why Rates Move

Most borrowers do not understand how oil prices, inflation, and Treasury yields connect to mortgage rates.

When you can explain the “why” behind rate movement, you position yourself as a trusted advisor.

- Do Not Wait for Perfect Rates

Rates may be improving, but volatility has not disappeared.

The brokers winning in this market are not waiting for perfect conditions. They are staying close to their pipeline and acting when opportunity windows open.

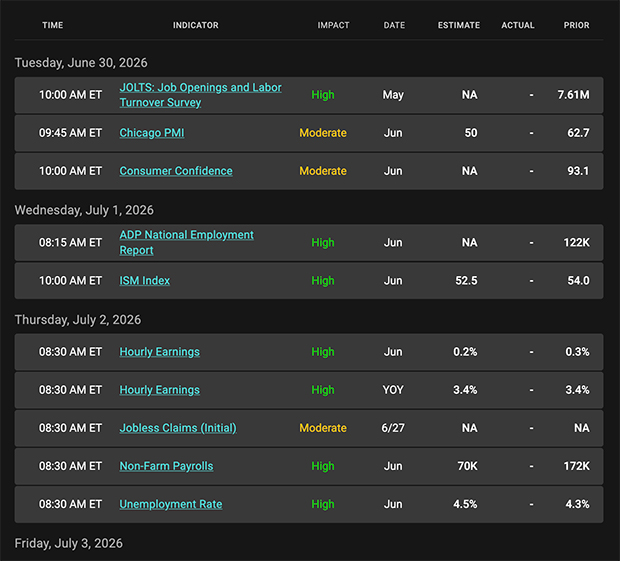

What Brokers Should Watch Next

Next week is a shortened holiday week, but there will still be important economic data.

Key reports include:

- JOLTS Job Openings

- ADP Employment Report

- ISM Manufacturing Index

- Weekly Jobless Claims

- Consumer Confidence

- Employment Report

Labor market data remains especially important because jobs support housing demand.

As the saying goes: jobs buy homes.

If the labor market stays strong while inflation continues to cool, that could support a more stable rate environment.

Bottom Line

Mortgage rates have improved, but the bigger story is what is driving the improvement.

Lower oil prices, lower diesel costs, easing inflation concerns, and a better Treasury trend are all helping mortgage rates move in a more favorable direction.

For mortgage brokers, this is a market to stay active in.

The brokers who understand what is driving rates — and communicate that clearly to borrowers — are the ones best positioned to turn market movement into real opportunity.

Mortgage Market Guide Candlestick Chart

Each candle represents one day of trading. As mortgage bonds prices move higher, rates move lower. You can see on the right side of the chart, how mortgage bond prices improved over the past several weeks in response to lower oil prices.

Chart: Fannie Mae 30-Year 5.5% Coupon (Friday, June 26, 2026)

Economic Calendar for the Week of June 29 – July 3

The material contained in this newsletter has been prepared by an independent third-party provider. The content is provided for use by real estate, financial services and other professionals only and is not intended for consumer distribution. The material provided is for informational and educational purposes only and should not be construed as investment and/or mortgage advice. Although the material is deemed to be accurate and reliable, there is no guarantee it is without errors.